SaaS valuation multiples in 2026 are more selective than they were during the growth-at-all-costs market.

ARR still matters. But investors are now looking more closely at growth quality, retention, profitability, AI defensibility and capital efficiency.

For SaaS CFOs and finance leaders, the message is clear:

- ARR growth is important, but it is no longer enough on its own.

- NRR, GRR, gross margin and Rule of 40 now carry more weight.

- Finance teams need metrics that explain both market performance and revenue quality.

This article summarises the latest 2026 SaaS valuation benchmarks and explains which metrics finance teams should track before a fundraise, board meeting or exit process

Key 2026 SaaS valuation takeaways

| 2026 takeaway | What it means for SaaS finance teams |

|---|---|

| Public SaaS multiples remain below pandemic-era levels | Do not assume 2021-style ARR multiples in fundraising or exit planning. |

| The market is more selective | Premium multiples are reserved for companies with stronger growth, retention and margins. |

| Rule of 40 matters again | Growth is being assessed alongside profitability and free cash flow. |

| NRR is a valuation lever | Strong expansion and low churn support higher revenue quality. |

| AI risk is affecting software valuations | Investors are reassessing product defensibility and long-term software moats. |

| Metrics quality matters | Investors need reliable ARR, revenue, churn and cohort reporting. |

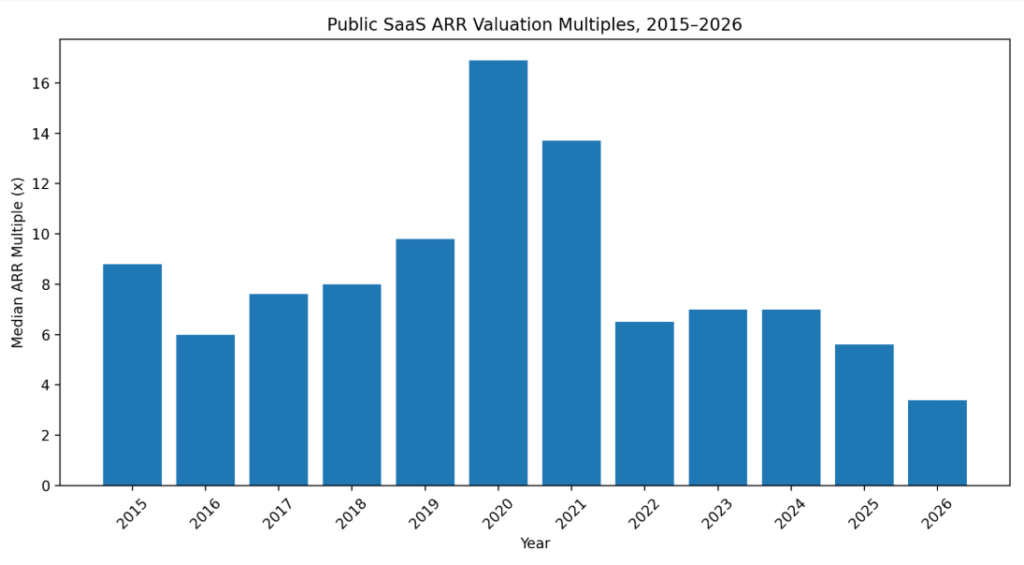

Current public benchmarks show the scale of the reset. The BVP Nasdaq Emerging Cloud Index currently shows an average revenue multiple around 6.2x and average revenue growth around 19.4%.

At the same time, SaaS Capital’s 2026 trends report notes that SaaS valuations hit decade-plus lows in Q1 2026 as markets priced in AI as a potential threat to traditional software models.

Valuation multiples are market-driven, but valuation readiness is finance-driven. SaaS finance teams need ARR, NRR, GRR, recognised revenue and deferred revenue to reconcile back to source data before board meetings, fundraising or exit diligence.

What is an ARR valuation multiple?

An ARR valuation multiple compares a SaaS company’s valuation with its annual recurring revenue.

| Example company | ARR | Valuation | ARR multiple |

|---|---|---|---|

| SaaS Company A | £10m | £50m | 5.0x ARR |

| SaaS Company B | £10m | £100m | 10.0x ARR |

ARR multiples are commonly used for SaaS companies because recurring revenue is one of the clearest indicators of future revenue visibility.

However, not all ARR is valued equally. Investors will usually apply a higher multiple to ARR that is growing quickly, retained well, generated efficiently and supported by strong margins.

For finance teams, this makes ARR reporting a board-level control issue. ARR should be traceable, explainable and consistent with customer, invoice and revenue data.

ScaleXP helps SaaS finance teams track ARR, MRR and revenue movement through finance-controlled reporting.

ARR multiple vs revenue multiple

ARR multiples and revenue multiples are often discussed together, but they are not always the same.

| Metric | What it uses | Common use |

|---|---|---|

| ARR multiple | Annual recurring revenue | SaaS fundraising, private SaaS valuation and subscription software benchmarks |

| Revenue multiple | Total revenue, run-rate revenue, LTM revenue or forward revenue | Public market comparisons, M&A benchmarks and broader software valuation |

| EV/revenue multiple | Enterprise value divided by revenue | Public company and M&A analysis |

| Market cap / ARR | Market value divided by annualised recurring revenue | Public SaaS index and ARR benchmark analysis |

When comparing SaaS valuation multiples, always check the definition. A 6x forward revenue multiple is not the same as a 6x ARR multiple based on current run-rate ARR.

The SaaS Capital Index calculates its ARR multiple as market capitalisation divided by annualised current run-rate revenue.

What are SaaS valuation multiples in 2026?

There is no single SaaS valuation multiple in 2026. The market is split by growth rate, company size, retention, profitability, product category and investor confidence.

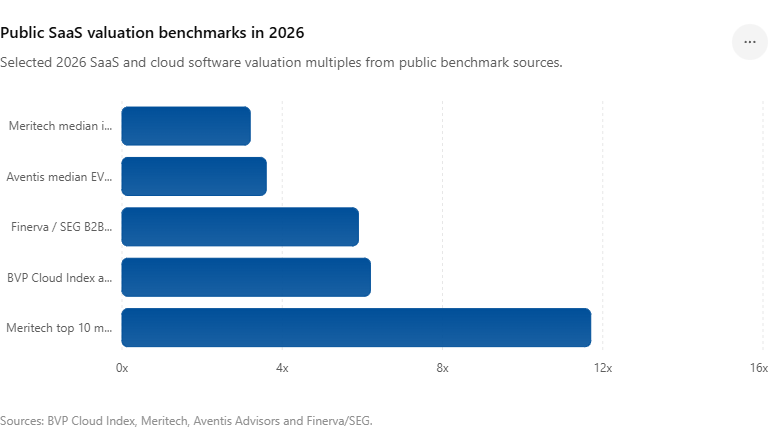

| Benchmark | 2026 reference point |

|---|---|

| BVP Nasdaq Emerging Cloud Index | Around 6.2x average revenue multiple |

| Meritech median public software | 3.2x median implied ARR multiple |

| Meritech top 10 public software companies | 11.7x median implied ARR multiple |

| Aventis Rule of 40 SaaS analysis | 3.6x median EV/revenue multiple |

| Finerva / SEG B2B SaaS benchmark | 5.9x B2B SaaS revenue multiple |

Current public SaaS benchmarks show a broad range:The important point is not the exact median on any single day. Public multiples move constantly.

The more useful question for finance leaders is: What makes one SaaS company deserve a higher ARR or revenue multiple than another?

Why SaaS valuation multiples changed in 2026

SaaS valuations in 2026 reflect a different investor mindset.

During 2020 and 2021, high growth and recurring revenue often attracted premium multiples, even where profitability was distant. By 2026, the market is more cautious. Growth still matters, but investors are asking harder questions about quality, efficiency and durability.

1. Growth has slowed

SaaS growth rates have normalised from the pandemic-era peak.

For many private SaaS companies, growth is now more moderate. SaaS Capital’s 2026 private B2B SaaS benchmark shows median revenue growth of 15% for bootstrapped SaaS companies with $3m to $20m ARR.

That does not mean growth is unimportant. It means investors are more focused on whether growth is efficient, repeatable and supported by retention.

2. AI has changed the software valuation debate

AI has created both opportunity and risk for SaaS companies.

Some companies are being rewarded for AI-native workflows or clear AI leverage. Others are being discounted where investors fear product commoditisation, weaker pricing power or disruption to traditional seat-based software models.

For CFOs, this increases the need to show clear evidence of durable customer value through retention, expansion, usage, gross margin and revenue quality.

3. Profitability and cash flow matter more

Rule of 40 has become a more visible valuation filter again.

A company growing at 40% with negative margins may be assessed very differently from a company growing at 20% with strong free cash flow. Investors want to understand both growth and the cost of achieving that growth.

4. Retention quality is under more scrutiny

A company with high ARR but weak retention will often receive a lower multiple than a company with the same ARR and stronger net revenue retention.

NRR and GRR help investors understand whether revenue is durable, expandable and less dependent on constant new customer acquisition.

5. Diligence standards are higher

Investors are spending more time testing whether reported metrics tell a consistent story.

They will not only ask whether ARR is growing. They will ask how that ARR moves by customer, how much is retained, how much is expanding, and how it connects to invoicing, revenue recognition and cash collection.

This makes valuation readiness a finance operating discipline, not just a fundraising exercise.

Public SaaS valuation multiples in 2026

Public SaaS companies provide the most visible benchmark for valuation multiples, but they are not a perfect proxy for private companies.

Public multiples are affected by stock market sentiment, interest rates, AI expectations, revenue growth, free cash flow, product category and company-specific performance.

As of 2026, public SaaS data shows three clear patterns.

1. Multiples are still below historic highs

The public SaaS market remains well below the valuation environment seen during the 2020–2021 peak.

Finance leaders should be cautious about using old fundraising decks or 2021 valuation benchmarks when planning a 2026 raise or exit.

2. The best companies still attract premium multiples

The gap between top-performing software companies and average software companies is wide.

Meritech’s 9 April 2026 Software Pulse reported a 3.2x overall median implied ARR multiple for public software, while the top 10 companies had a median implied ARR multiple of 11.7x.

This is a clear reminder that “SaaS company” is no longer enough to earn a premium multiple. The strongest companies are separating from the median.

3. The median company is being valued more cautiously

Median public SaaS multiples are much lower than top-quartile multiples.

That means private companies should avoid anchoring valuation expectations to the best public software companies unless their own metrics are genuinely comparable.

Private SaaS valuation multiples in 2026

Private SaaS valuations are harder to benchmark because funding rounds and M&A transactions are not always public.

For private companies, ARR multiples usually depend on:

- ARR scale

- ARR growth rate

- Net revenue retention

- Gross revenue retention

- Gross margin

- EBITDA or free cash flow margin

- Customer concentration

- Market category

- Product defensibility

- Investor demand

- Quality of financial reporting

A private SaaS company with £5m ARR, 35% growth, strong NRR and breakeven margins may command a very different multiple from a company with the same ARR but flat growth, weak retention and messy revenue data.

The Finerva B2B SaaS 2026 valuation multiples report reports that B2B SaaS revenue multiples recovered to 6.7x in 2024, then contracted to 5.9x in 2025.

This is why finance teams should prepare more than one benchmark. Use public SaaS indices for context, private SaaS benchmarks for peer comparison, and company-specific metrics to support the valuation story.

What increases a SaaS company’s valuation multiple?

SaaS valuation is not driven by ARR alone. The highest-quality ARR usually has five characteristics:

- It is growing.

- It is retained.

- It expands.

- It has strong gross margin.

- It can be reported accurately.

Key valuation drivers for SaaS companies

| Valuation driver | Why it matters | Metrics to track |

|---|---|---|

| ARR growth | Shows market demand and revenue momentum | ARR, new ARR, expansion ARR |

| Net revenue retention | Shows whether customers expand or contract | NRR, expansion, contraction, churn |

| Gross revenue retention | Shows durability before upsell | GRR, logo churn, revenue churn |

| Gross margin | Shows scalability of the business model | Revenue, COGS, gross margin by customer/product |

| Rule of 40 | Balances growth and profitability | Revenue growth plus EBITDA or FCF margin |

| CAC payback | Shows sales efficiency | CAC, new ARR, gross margin-adjusted payback |

| Revenue quality | Reduces diligence risk | Recognised revenue, deferred revenue, accrued revenue |

| Forecast visibility | Supports investor confidence | Forecast ARR, renewals, pipeline, bookings |

| Customer concentration | Shows dependency risk | ARR by customer, top 10 customer concentration |

| Reporting confidence | Shows whether management can explain the numbers under review | Reconciled ARR movements, board pack metrics, source-system checks |

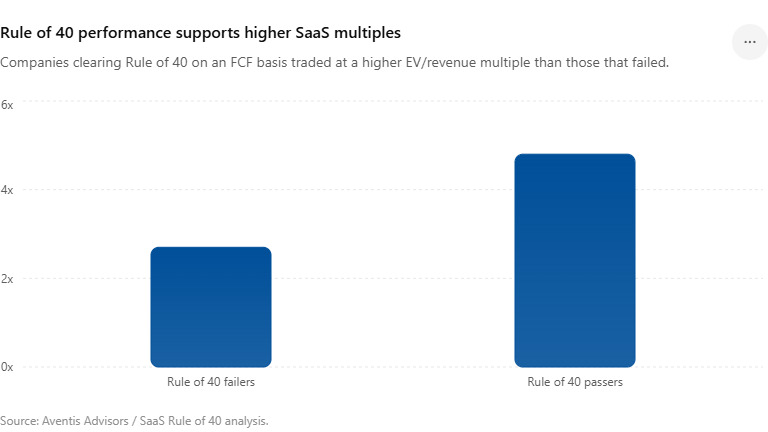

Rule of 40 and SaaS valuation multiples

Rule of 40 is a simple measure used by investors to assess the balance between growth and profitability.

The formula is:

Revenue growth rate + profit margin = Rule of 40 score

Profit margin may be measured using EBITDA margin, operating margin or free cash flow margin, depending on the investor or benchmark.

For example:

| Revenue growth | EBITDA margin | Rule of 40 score |

|---|---|---|

| 30% | 10% | 40% |

| 20% | 20% | 40% |

| 50% | -10% | 40% |

| 15% | 5% | 20% |

A company above 40% is generally considered to have a healthier balance of growth and profitability. A company below 40% may still be attractive, but investors will look more closely at the reason.

In 2026, Rule of 40 is especially important because many SaaS companies are growing more slowly than they did during the pandemic-era software boom. That makes margin, efficiency and cash generation more important parts of the valuation story.

Aventis Advisors’ 2026 Rule of 40 analysis reports that only 8 of 55 listed SaaS companies, or 15%, cleared the Rule of 40 on an EBITDA basis. The same analysis reported a mean EV/revenue multiple of 4.7x and a median EV/revenue multiple of 3.6x.

NRR and SaaS valuation multiples

Net revenue retention is one of the most important SaaS valuation metrics.

NRR measures how revenue from existing customers changes after expansion, contraction and churn.

A company with high NRR can grow even before adding new customers. That is attractive because it shows that the existing customer base is expanding and that the product has continued value.

Why NRR matters to valuation

| NRR result | What it suggests |

|---|---|

| Below 100% | Existing customer revenue is shrinking |

| Around 100% | Expansion offsets contraction and churn |

| Above 110% | Existing customers are expanding meaningfully |

| Above 120% | Strong expansion motion, often seen in higher-quality SaaS companies |

NRR should not be viewed in isolation. A company can have strong NRR but weak gross revenue retention if upsell hides churn. Investors will usually review both NRR and GRR.

ScaleXP helps finance teams track retention, expansion and churn from source data.

GRR and SaaS valuation multiples

Gross revenue retention measures how much recurring revenue is retained before expansion.

It answers a different question from NRR:

- NRR asks: “Are customers expanding overall?”

- GRR asks: “How much revenue are we keeping before upsell?”

A company with high NRR but low GRR may still have a churn problem. A company with strong GRR has a more durable base of recurring revenue.

For valuation purposes, strong GRR reduces perceived risk. It shows that revenue is less dependent on replacing lost customers or constantly finding expansion revenue.

Revenue recognition and valuation readiness

Revenue recognition is often overlooked in SaaS valuation discussions.

That is a mistake.

ARR and revenue are not the same thing. A SaaS company may invoice annually, recognise revenue monthly and carry a deferred revenue balance on the balance sheet. If those movements are not clear, the financial statements can appear disconnected from commercial performance.

Before a fundraise or exit process, finance teams should be able to explain:

- ARR and MRR movement

- New, expansion, contraction and churned ARR

- Recognised revenue

- Deferred revenue

- Accrued revenue or unbilled revenue

- Revenue by product, customer or entity

- CRM pipeline and renewal assumptions

- Forecast revenue and cash impact

Clean revenue recognition does not automatically increase a valuation multiple. But it does reduce friction during diligence by making the link between contracts, invoices, revenue and reported SaaS metrics easier to explain.

ScaleXP helps finance teams automate revenue schedules, recognised revenue, deferred revenue and revenue journals. Learn more about ScaleXP’s revenue recognition software.

Deferred revenue and SaaS valuation

Deferred revenue is an important part of SaaS valuation readiness because it explains the gap between invoicing, cash collection and recognised revenue.

Many SaaS companies invoice annually or upfront. That creates cash, but it does not mean all revenue can be recognised immediately. The unrecognised portion is carried as deferred revenue.

Investors may review deferred revenue to understand:

- How much revenue has been invoiced but not yet recognised

- Whether revenue schedules are accurate

- Whether revenue recognition is consistent

- Whether cash collection and revenue recognition are properly separated

- Whether reported ARR aligns with contract and billing data

Finance teams should be able to reconcile deferred revenue to invoices, customer contracts and recognised revenue. This becomes especially important during fundraising, audit or exit diligence.

ScaleXP helps finance teams automate deferred revenue schedules and reporting. Learn more about ScaleXP’s deferred revenue software.

SaaS metrics investors expect before fundraising

Before a fundraising process, SaaS CFOs should prepare a metrics pack that reconciles to source systems.

| Metric | Why investors ask for it |

|---|---|

| ARR | Core recurring revenue base |

| MRR | Monthly recurring revenue trend |

| New ARR | New customer acquisition momentum |

| Expansion ARR | Growth from existing customers |

| Contraction ARR | Downgrades and customer spend reduction |

| Churned ARR | Lost recurring revenue |

| NRR | Net expansion or contraction from existing customers |

| GRR | Revenue retained before expansion |

| CAC payback | Sales and marketing efficiency |

| Gross margin | Scalability of the revenue base |

| Rule of 40 | Balance of growth and profitability |

| Deferred revenue | Invoiced but not yet recognised revenue |

| Recognised revenue | Revenue recorded under accounting rules |

| Forecast ARR | Forward-looking recurring revenue visibility |

The strongest SaaS finance teams do not prepare these metrics manually at the last minute. They maintain them monthly, reconcile them to source data and use them in board reporting.

How ScaleXP helps SaaS companies prepare investor-ready metrics

ScaleXP helps SaaS finance teams connect accounting, billing and CRM data so revenue metrics can be reviewed from one finance-controlled dataset.

Finance teams use ScaleXP to track SaaS metrics, revenue recognition, deferred revenue, forecasts and board reporting without rebuilding spreadsheets each month.

ScaleXP helps teams:

- Track ARR, MRR, NRR, churn and expansion from source data.

- Connect revenue metrics to Xero, QuickBooks, Stripe, HubSpot or Salesforce workflows.

- Reconcile SaaS metrics with recognised, deferred and accrued revenue.

- Automate deferred revenue schedules and revenue journals.

- Build board-ready reporting packs from finance-controlled data.

- Improve auditability before fundraising, board meetings or exit diligence.

This matters because valuation conversations are not only about growth. They are also about whether the reported metrics can be trusted.

Book a demo to see ScaleXP’s SaaS metrics and revenue reporting workflow.

Example: why two SaaS companies with the same ARR can have different valuations

Two companies may both have £10m ARR, but receive very different valuations.

| Metric | Company A | Company B |

|---|---|---|

| ARR | £10m | £10m |

| ARR growth | 12% | 35% |

| NRR | 96% | 118% |

| GRR | 82% | 94% |

| Gross margin | 68% | 82% |

| Rule of 40 | 10% | 42% |

| Revenue reporting | Manual spreadsheets | Reconciled monthly |

| Investor confidence | Lower | Higher |

Company B is likely to command a higher valuation multiple because its revenue is growing faster, retained better and supported by stronger financial discipline.

This is why SaaS CFOs should not focus only on the headline multiple. The quality of the underlying metrics matters.

How to prepare your SaaS company for valuation discussions

Finance teams can improve valuation readiness long before a formal fundraise or exit process.

1. Reconcile ARR to source data

ARR should not be a standalone spreadsheet number. It should be traceable to customer contracts, invoices, billing data or CRM data.

2. Track expansion, contraction and churn separately

Investors want to understand the movement in ARR, not just the closing balance.

3. Review NRR and GRR every month

NRR shows expansion quality. GRR shows revenue durability. Both matter.

4. Connect revenue recognition to SaaS metrics

ARR, invoices and recognised revenue should tell a consistent story.

5. Prepare Rule of 40 reporting

Track growth and profitability together. Do not wait until a board meeting or investor request.

6. Build board reporting from repeatable data

If every board pack requires manual spreadsheet work, the risk of errors increases. Repeatable reporting improves confidence.

Common mistakes in SaaS valuation benchmarking

Using old 2021 multiples

The software market has changed. Historic peak multiples are not a reliable benchmark for 2026.

Comparing private companies directly to top public companies

Top public SaaS companies often have scale, liquidity, brand strength and investor access that private companies do not.

Ignoring retention

ARR growth driven by new sales can hide churn. Investors will look at NRR and GRR.

Treating ARR as revenue

ARR is a recurring revenue measure. It is not the same as recognised revenue under accounting standards.

Reporting metrics from disconnected spreadsheets

Manual metrics can work early on, but they become harder to defend as the business scales or enters diligence.

SaaS valuation multiples in 2026: summary for CFOs

SaaS valuation multiples in 2026 are more disciplined than in the pandemic-era market.

The companies best positioned for premium multiples are not simply those with the highest ARR. They are the companies that can show:

- Durable recurring revenue

- Strong ARR growth

- High NRR and GRR

- Clear gross margin

- Efficient customer acquisition

- Rule of 40 progress

- Clean revenue recognition

- Reliable, reconciled SaaS metrics

For SaaS finance leaders, the job is not to guess the perfect valuation multiple. It is to build the reporting foundation that allows investors, boards and acquirers to trust the numbers.

ScaleXP helps SaaS finance teams connect accounting, CRM and billing data so ARR, revenue recognition, deferred revenue and board reporting are easier to manage, review and explain.

See ScaleXP’s SaaS metrics reporting in action.

FAQs: SaaS ARR and revenue valuation multiples in 2026

A good ARR multiple for a SaaS company in 2026 depends on growth, retention, profitability, company size and product category. Median public SaaS multiples are far below the 2021 peak, while top-performing companies with strong ARR growth, high NRR and Rule of 40 performance can still achieve premium valuations.

An ARR multiple compares company valuation with annual recurring revenue. A revenue multiple may use total revenue, trailing revenue, forward revenue or annualised run-rate revenue. For SaaS companies, ARR multiples are useful because they focus on recurring subscription revenue, but the exact definition should always be checked before comparing benchmarks.

SaaS valuation multiples are lower in 2026 because investors are applying more scrutiny to growth, profitability, AI defensibility and revenue quality. Growth alone is no longer enough. Investors now look more closely at NRR, GRR, gross margin, Rule of 40, cash efficiency and the reliability of reported SaaS metrics.

Rule of 40 affects SaaS valuation because it shows the balance between growth and profitability. A SaaS company with strong revenue growth and positive EBITDA or free cash flow margins may command a higher valuation multiple than a company with similar ARR but weaker efficiency. Rule of 40 is especially important when growth rates slow.

NRR, or net revenue retention, affects SaaS valuation because it shows whether existing customers are expanding, contracting or churning. Higher NRR usually supports a stronger valuation because it indicates durable revenue, customer expansion and lower reliance on new customer acquisition. Investors often review NRR alongside GRR.

Public SaaS valuation multiples are useful as a reference point, but they should not be applied directly to private companies. Private SaaS valuations also depend on ARR scale, growth rate, retention, gross margin, profitability, customer concentration, product category, investor appetite and the quality of financial reporting.

Before fundraising, SaaS CFOs should prepare ARR, MRR, new ARR, expansion ARR, contraction ARR, churned ARR, NRR, GRR, CAC payback, gross margin, Rule of 40, deferred revenue, recognised revenue and forecast ARR. These metrics should be consistent with source data from accounting, billing and CRM systems.